One of the first long-term thoughts many Muslim parents have after a child is born is simple: I want their life to be easier than mine.

In the United States, that thought quickly turns into a practical question — education, training, and early adulthood all require money, and many parents feel pressure to begin saving immediately.

Muslim parents often face additional uncertainty: are education savings accounts halal, can a 529 plan be used, and how should investments be handled responsibly?

Browse and compare halal investing platforms to find the right fit for your portfolio.

This guide explains the main saving options clearly so you can make a thoughtful decision without delaying planning.

Ready to compare halal options?

You Do Not Need to Panic

Many parents feel they must immediately save large amounts. In reality, the most important factor is not how much you start with — it is how early you begin.

Not sure where to begin? Get matched with a halal investing platform in 60 seconds.

Small, consistent contributions made early often matter more than large contributions started years later because time allows investments to grow.

The Three Main Saving Structures

Families in the U.S. typically save for children using three structures: 529 education plans, custodial investment accounts (UTMA/UGMA), or parent-owned investment accounts.

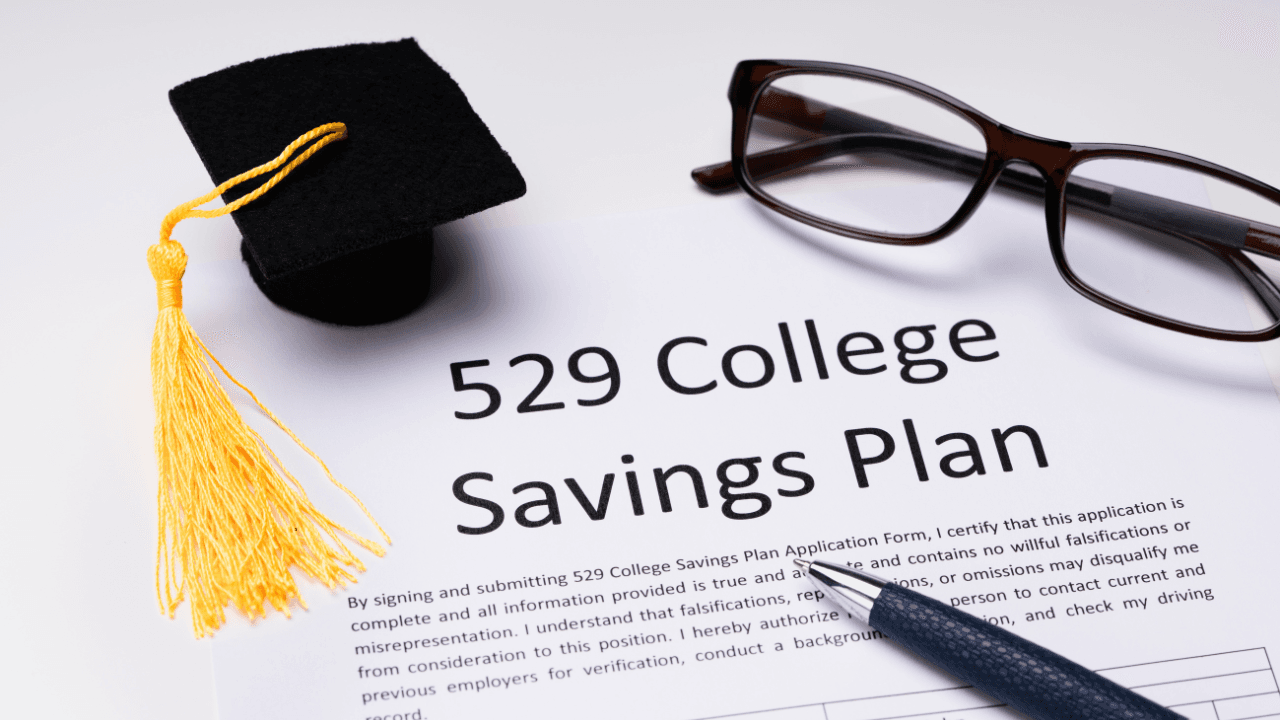

Option 1 — 529 Education Plans

A 529 plan is a tax-advantaged education savings account where investments grow tax-free and withdrawals for qualified education expenses are tax-free.

The Islamic concern is not the account itself but the investments inside it. Standard mutual funds may include interest-based businesses or impermissible industries.

Explore our guide to halal ETFs available to U.S. investors.

The permissibility depends on what the funds invest in. Some parents carefully choose screened or conservative portfolios when available.

Option 2 — Custodial Accounts (UTMA/UGMA)

Top Providers for This Topic

Free to compare · No sign-up required

Custodial accounts allow parents to invest directly in the child’s name. Parents can buy individual stocks or halal-screened ETFs and actively manage investments.

Advantages include greater control over investment choices and the ability to ensure halal screening. However, the child gains legal ownership when they reach adulthood.

Option 3 — Investing in a Parent-Owned Account

Some families invest within their own brokerage account and designate a portion for their child. This provides flexibility and avoids transferring legal ownership at a fixed age.

Islam does not require funds to be held in the child’s name — the responsibility is to provide responsibly.

Interest Concerns

The primary issue is how the money is invested, not the act of saving. Muslim families often select screened funds, Shariah-compliant ETFs, or carefully chosen stocks.

Related reading: Beginner Investing Guide for Muslims · What Makes a Stock Halal · Shariah Stock Screening Guide

Islamic financial screening recognizes that modern markets are complex and encourages reasonable effort rather than perfection.

A Common Mistake

Many parents delay saving while searching for the perfect solution. Waiting often costs more than beginning with a simple approach and improving over time.

How Much Should You Save?

The goal is not necessarily to fully fund education but to create options. Even partial savings can reduce loans and increase flexibility.

Consistent monthly saving, even modest amounts, can grow significantly over many years.

The Islamic Perspective

Compare providers in your state

See side-by-side comparisons of Shariah-compliant products, or let our matcher recommend the best options for your situation.

Islam does not require parents to leave wealth but encourages not leaving dependents financially vulnerable. Saving for a child’s future is responsible preparation.

Providing a financial starting point helps protect dignity and opportunity, which is the true objective of long-term saving as a parent.