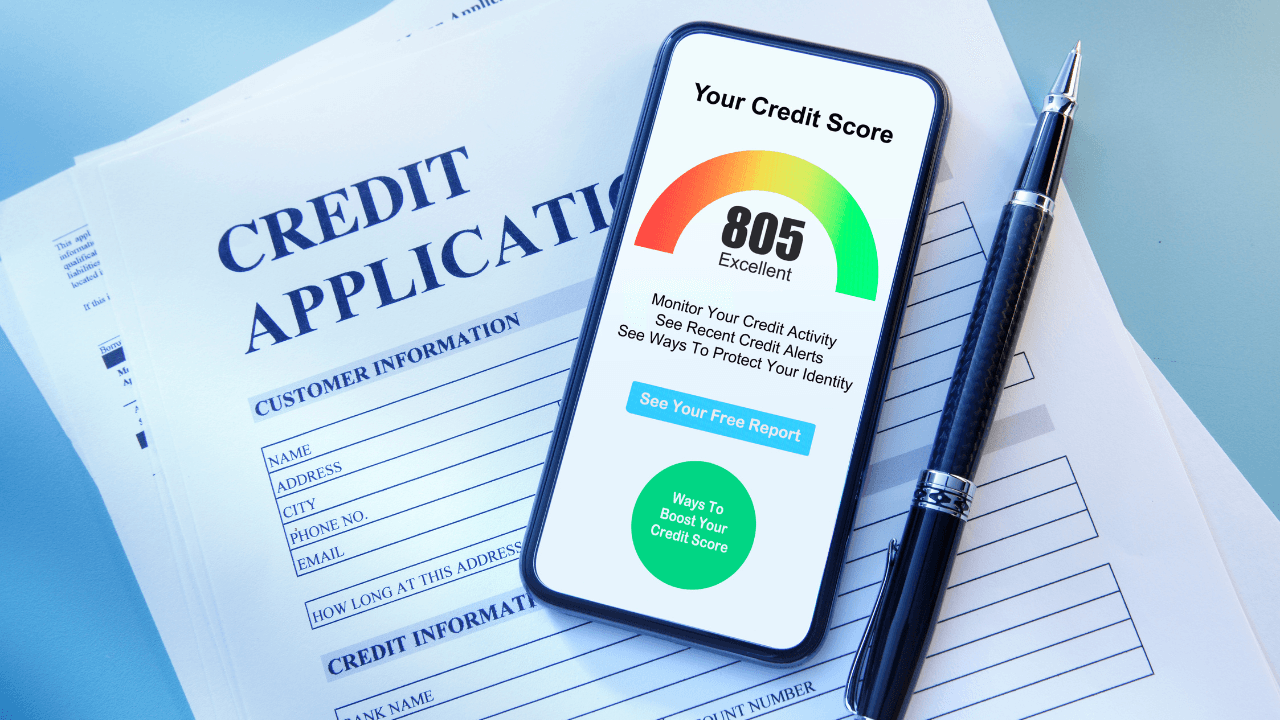

One of the most common questions Muslim homebuyers have before applying for halal financing is whether their credit score is good enough. The short answer: halal lenders use the same credit scoring system as conventional lenders. A 720 gets you better terms whether you're applying to Guidance Residential or Chase. The difference is that halal lenders have their own specific thresholds and some flexibility in how they look at the full picture.

This guide covers what credit scores each major halal provider looks for, why your score matters beyond the minimum, and what to do if your score needs work before you apply.

Ready to compare halal options?

How credit scoring works for halal mortgage applications

U.S. halal home financing providers use FICO scores, pulled from one or more of the three major credit bureaus (Equifax, Experian, TransUnion). The scoring range is 300 to 850. Most lenders use the middle score across all three bureaus when making a decision.

Your credit score affects two things: whether you qualify at all, and what terms you receive. Qualification is a binary question with a threshold. Terms are a sliding scale where a higher score gets you better pricing and more flexibility.

Islamic financing agreements don't use an interest rate in the same way conventional mortgages do, but the equivalent pricing (the profit rate, rental rate, or cost-plus markup) is still influenced by credit quality. A buyer with a 750 will generally get better terms than a buyer with a 640, even if the structure of the agreement looks different.

Credit score requirements by halal lender

Guidance Residential generally requires a minimum credit score of around 620 for standard programs. Their most competitive pricing tiers typically require scores above 700. They're the largest U.S. halal home financing provider by volume and have experience working with buyers across a wide range of credit profiles.

Ijara CDC also has a minimum credit score threshold in the 620 to 640 range for most programs, though specific requirements vary by state and program type. Their 33-state footprint means credit requirements may differ slightly depending on your location.

University Islamic Financial (UIF) and Neeyah have their own credit thresholds. As with any lender, requirements change over time, so verify directly before applying. The halal home financing hub has an overview of the major providers if you want to compare before contacting them.

What else halal lenders look at beyond your score

Credit score is one piece of the picture. Halal lenders, like conventional ones, also look at:

Debt-to-income ratio (DTI): Your monthly debt payments divided by your gross monthly income. Most lenders want to see a DTI below 43%, with some flexibility to 50% for strong applications. High debt relative to income can offset a good credit score.

Employment history: Two years of stable employment in the same field is the standard benchmark. Self-employed borrowers typically need two years of tax returns showing consistent income.

Payment history: Even if your score is strong, recent late payments on your report can be a problem. A single late payment from 3 years ago is very different from a late payment from 6 months ago.

Down payment and reserves: How much you're putting down and how much you have left in savings after closing. Lenders want to see you won't be completely depleted post-purchase. Having 2 to 3 months of payments in reserves after closing strengthens a borderline application.

The Muslim credit score challenge

Some Muslim homebuyers have lower-than-expected credit scores specifically because they've avoided conventional credit products on religious grounds. No credit cards, no conventional car loans, no conventional mortgages. The problem: credit scores are built through credit history, and if you've never used credit, you may have a thin file or no score at all.

Top Providers for This Topic

Free to compare · No sign-up required

This is a real and documented issue in the Muslim community. The good news: there are ways to build credit without using interest-bearing products that conflict with Islamic principles. A secured credit card paid in full every month builds credit without you carrying a balance or paying interest. Being added as an authorized user on a family member's account with a strong payment history can lift your score. Some halal lenders also do manual underwriting for buyers with thin credit files, looking at rent payment history, utility payments, and other non-traditional indicators.

How to improve your credit score before applying

If you're 6 to 12 months away from wanting to apply, there are specific moves that reliably improve credit scores:

Pay every bill on time, every month. Payment history is the single largest factor in your credit score (35% of the FICO calculation). One missed payment can set you back significantly. Set up autopay for minimums on any credit accounts as a safety net.

Bring credit card utilization below 30%. The ratio of how much you owe on revolving credit versus your credit limit is the second largest factor (30% of FICO). If you have a $5,000 credit limit and a $3,000 balance, your utilization is 60%, which drags your score. Pay that balance down before applying.

Don't open new accounts in the months before applying. Each new credit application creates a hard inquiry on your report, which temporarily lowers your score. Avoid opening new cards, buying a car on credit, or taking out any new loans in the 6 to 12 months before your mortgage application.

Check your credit reports for errors. Get your free reports from all three bureaus and look for accounts that aren't yours, incorrect payment statuses, or duplicate entries. Dispute any errors. This is a surprisingly common way to pick up 20 to 40 points quickly.

What to do if your score is below the minimum

If you're below 620, you're not ready to apply yet. That's not a dead end. It's a 6 to 18 month project. Build a plan: address any derogatory marks on your report, pay down revolving balances, and establish consistent payment history. Most negative items age off or lose impact over time, and 18 months of clean payment history does meaningful work.

Some halal lenders also offer program options for buyers with non-traditional credit histories. If you have no credit history but a strong record of on-time rent and utility payments, it's worth asking whether a provider will consider that in a manual underwriting review.

Frequently asked questions

Does applying to multiple halal lenders hurt my credit score?

Mortgage inquiries are treated differently from credit card or auto loan inquiries. Credit bureaus recognize rate shopping and generally count multiple mortgage inquiries within a 14 to 45 day window as a single inquiry. So applying to Guidance Residential and Ijara CDC within the same month shouldn't meaningfully damage your score. Get your applications in close together to take advantage of this window.

Can I get a halal mortgage with no credit history at all?

It's difficult but not always impossible. Some halal lenders will do manual underwriting for buyers with thin or no credit files, looking at rent payment history, utility payments, bank account history, and employment stability. Contact Guidance Residential or Ijara CDC directly to ask whether they have a manual underwriting path if you're in this situation.

Will avoiding conventional credit products prevent me from ever qualifying for halal financing?

Not necessarily, but it does make the path harder. The most halal-compatible way to build credit is through a secured credit card paid in full every month (no interest charged if you pay the full balance). This builds credit history without involving riba in any meaningful way, since you're not borrowing money or paying interest. That's the most commonly recommended approach within the Muslim community for this exact situation.

Compare providers in your state

See side-by-side comparisons of Shariah-compliant products, or let our matcher recommend the best options for your situation.

Is a 680 credit score good enough for halal financing?

680 is above most minimum thresholds and should qualify you for standard programs at Guidance Residential and Ijara CDC. You likely won't receive the best available terms at 680, but you should be able to get a financing agreement in place. Above 700 typically opens better pricing. Above 740 is where the best terms become available across most lenders.